What begins as a request for a “loan” may actually be a hope for a gift. Before you decide how to help, it’s worth understanding the differences between gifting and lending, and how each approach affects your finances, your taxes, and your long‑term planning. For families managing significant wealth, these decisions also connect to broader goals such as multigenerational planning, stewardship, and maintaining family harmony. Understanding the structure behind each option can help you offer support in a way that aligns with both your values and your long‑term financial strategy.

Here are some key considerations behind each option so you can choose the structure that best supports both your family member and your broader financial goals.

Understanding What It Means to Gift

A gift is an irrevocable transfer of wealth. Once given, it cannot be reclaimed, and there is no expectation of repayment. For many families, gifting is a simple and heartfelt way to offer support while potentially reducing the size of one’s taxable estate over time.

Key considerations when gifting:

- Annual exclusion limits apply: In 2026, you may give up to $19,000 per donor, per recipient without filing a gift tax return.

- Married couples can combine gifts: Two spouses may each give $19,000 to the same person, allowing $38,000 per recipient.

- Married couple gifting to another married couple expands the opportunity to $76,000 in a single year.

- Timing can increase impact. Making gifts in December and again in January of the following year allows you to transfer roughly $152,000 in a short window without filing Form 709.

- Form 709 is informational. Filing does not mean you owe tax; it simply tracks gifts above the annual exclusion against your lifetime exemption.

- Generally, personal gifts are not deductible by the donor and not taxable income for the recipient.

Gifting can also support long‑term intentions, such as helping adult children build financial stability, encouraging responsible decision‑making, or gradually transferring assets in a way that feels thoughtful and fair. Some families also coordinate gifts with existing estate planning structures to keep everything aligned.

Understanding What It Means to Lend

An intra‑family loan is a formal loan between family members. Unlike a gift, a loan creates a legal obligation to repay, and it must include interest at or above the IRS‑published Applicable Federal Rate (AFR).

Key considerations when lending:

- A written agreement is required: An attorney can draft the contract, though simple loans can be documented without one.

- Interest must meet AFR standards: The IRS publishes short‑term, mid‑term, and long‑term AFRs monthly. Charging less than the AFR may create a taxable gift.

- No gift tax return is required if the loan uses AFR‑compliant interest.

- Interest received is taxable income to the lender.

- Interest paid may be deductible for the borrower in certain circumstances (e.g., qualified home acquisition debt).

- Repayment terms can be flexible as long as they are documented and followed.

Intra‑family loans can help a family member access capital at a lower cost than a commercial loan while preserving your ability to be repaid.

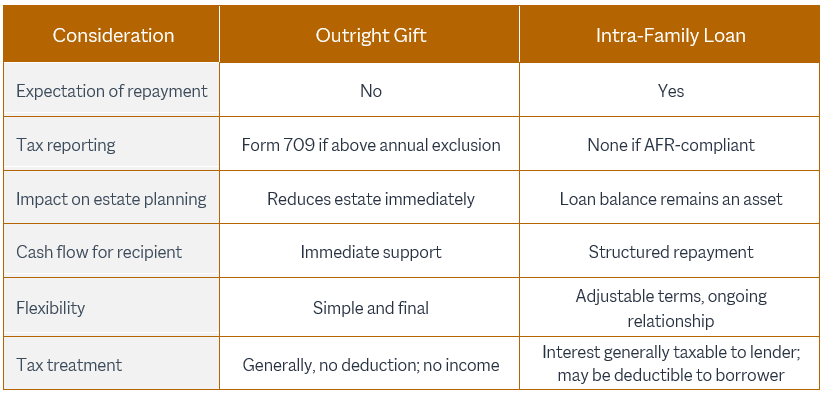

Comparing Options at a Glance

Blending Strategies: Using Gifting to Support Loan Repayment

Depending on a family’s circumstances, a combined approach may be an effective strategy. A lender may choose to gift the annual exclusion amount to the borrower each year, who then uses those funds to make interest or principal payments on the loan.

This approach can help:

- Maintain the clarity of a formal loan

- Support the borrower’s cash flow

- Allow the lender to continue transferring wealth gradually

This can also help keep support balanced among family members, especially when different children or relatives have different needs at different times.

Maintaining Clarity and Family Harmony

When money moves within a family, clarity matters. A few simple steps can help avoid misunderstandings later:

- Put agreements in writing so everyone understands the expectations.

- Communicate openly about the purpose and structure of the support.

- Coordinate gifts or loans with your broader estate plan.

- Consider how support for one family member fits into your long‑term intentions for the whole family.

These small steps can go a long way toward helping to preserve trust and harmony. Additionally, to preserve the integrity of the loan, the annual gift should be made without conditions, and loan payments should continue to be made according to the promissory note.

Choosing the Approach That Fits Your Intentions and Goals

Giving financial support works best when the structure fits comfortably within your broader financial life. It can help to think about how the support affects your cash flow, where the funds should come from, and how the choice aligns with your long‑term goals. It’s also worth considering whether you expect repayment, how much structure you want to put in place, and the recipient’s ability to manage the approach you choose. A bit of planning can help ensure that your generosity remains clear, sustainable, and supportive of the future you envision.

If you’d like to explore how these approaches might work in your situation, we’re here to help you think it through.