This rate has come down from a cycle peak above 5%, following cuts made in late 2024 and through 2025.[1] Most market participants guessed that a rate cut was not in the cards for this meeting, coming on the heels of higher headline inflation and relatively strong labor numbers. While core inflation in May (which doesn’t include food and energy) was only modestly higher, headline inflation was pushed higher in part by rising energy prices, amid geopolitical tensions involving Iran.[2] In addition, the May jobs report revealed an increase in nonfarm payrolls (NFP) and a steady unemployment rate of 4.3%. [3]These factors together reduced the likelihood of a near-term rate cut and, in the view of some market participants, left open the possibility of a further increase later this year.

Investors had been awaiting the first meeting for new Federal Reserve Chairman Kevin Warsh with bated breath. We addressed this changing of the guard in a previous publication, Investor Brief: Musical (Fed) Chairs, noting that, “recently he has aligned with arguments for faster rate cuts, asserting that productivity gains could support growth without triggering inflation.” When Warsh was nominated, many observers questioned how independent his policy stance would be once in office. However, the recent decision suggests that the committee remains focused on incoming economic data.

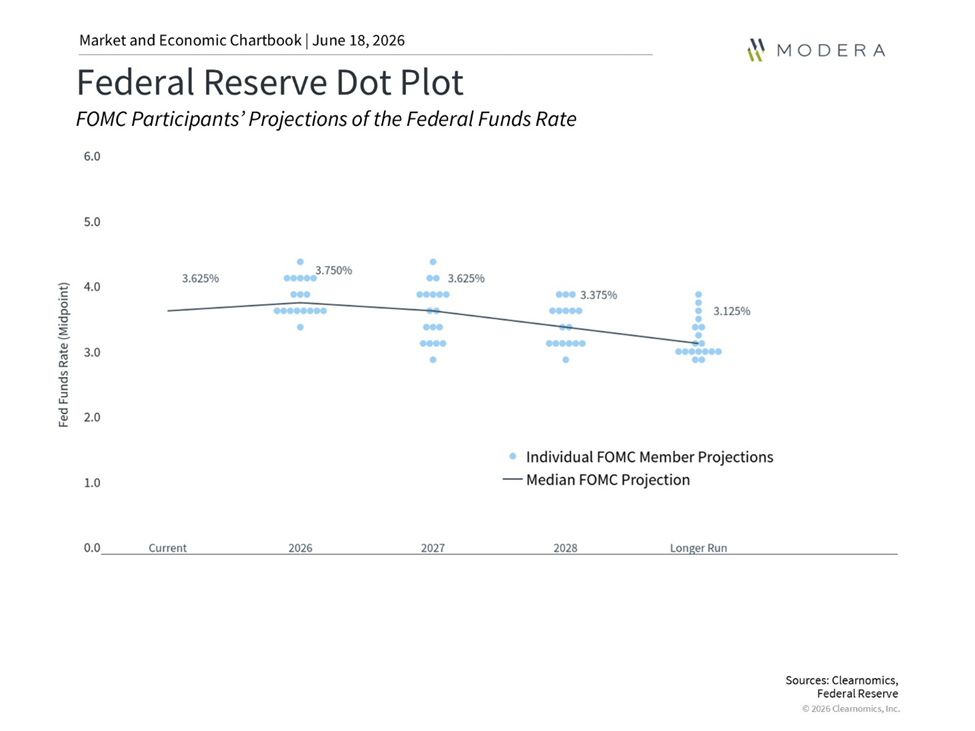

While the committee’s rate decision was widely anticipated, the meeting was interesting for a different reason: namely, what the committee didn’t say. For most of this century, the FOMC has provided forward guidance language in their post-meeting policy statements. At the press conference, Warsh noted that this committee’s statement was shorter, simpler, and omitted “forward guidance, which we agreed was not well-suited to the current policy conjecture.”[1] And while they did release the Summary of Economic Projections (SEP), also known as the Dot Plot, Warsh refrained from offering his own rate projections as part of the SEP.

For a statement with fewer words than usual, it’s a lot to unpack. But without the need to provide explicit forward guidance, Warsh appears to give the committee the flexibility to ingest and consider the economic data as it unfolds, and adjust to changing circumstances as they see fit. It remains to be seen how markets handle the decreased communication regarding forward guidance. The dot plot that was released indicated that 9 of 18 participants penciled in the potential for a rate hike by year-end, which was enough to lead markets lower on the day, though they reversed course the following day as investors reacted to easing geopolitical concerns. [1]

The direction of the FOMC under a new chair is certainly interesting, with the recent meeting hinting as to how the committee will handle monetary policy in this new era. However, from an investing perspective there were no actionable takeaways for portfolios at this time. We continually monitor market and economic conditions and consider their impact on our allocations, which are designed with diversification and long-term risk objectives in mind. As always, we will keep a close eye on the economic data and the Fed’s Summary of Economic Projections – minus one dot.