When my daughters were young, they loved going to the drive-in movies during the summer. There was something special about being outdoors under the stars, with crickets chirping, the radio crackling, and the scents of popcorn, hot dogs, and fried dough all around. They would create a cozy bed out of what seemed to be every blanket in the house. Suddenly, the biggest screen a child could imagine lit with color, lights, and movement, the ensuing magic capturing their rapt attention.

Those summer evenings at the drive-in came to mind recently when I was asked how I would describe today’s investment markets. Oddly enough, I thought of the movie “Mary Poppins.” Don’t ask me why, but my gut reaction was to say that today’s markets are supercalifragilisticexpialidocious. If you remember “Mary Poppins,” you are familiar with that word. Even though the sound of it is something quite atrocious, it is as good a descriptor as I can think of to summarize the current economic situation.

Like the infamous word, not everything meaningful is easy to explain. Investing works the same way. Short-term swings are noisy, emotional, and can be unsettling. We are constantly navigating so many uncertainties: interest rates, geopolitics, oil, inflation, and artificial intelligence, to name a few. However, while these uncertainties may fuel short-term volatility, they rarely change the long-term drivers of wealth creation.

Supercalifragilisticexpialidocious stands out because it makes little sense; long-term investing stands out because it does. Investing isn’t about finding magic. Rather, it’s about adhering to key principles. Disciplined, patient investors who stay focused on quality, innovation, earnings growth, diversification, and the power of compounding are typically rewarded over time.

When uncertainty dominates the conversation, maintaining perspective is often the most valuable investment strategy of all.

Markets

The first half of the year was a good reminder that markets rarely move in a straight line. The first quarter was dominated by geopolitical tensions, tariff concerns, sticky inflation, and talk of Federal Reserve rate cuts. That uncertainty weighed most heavily on U.S. large-cap growth stocks, while value stocks and smaller companies held up relatively better. International markets were mixed, and bond returns were modest as interest rates moved higher.

The second quarter told a very different story. Investor sentiment appeared to improve as corporate earnings remained resilient, the U.S. economy continued to expand, and fears of a meaningful economic slowdown eased. Markets focused on healthy earnings growth and the longer-term benefits that artificial intelligence and business investment may provide. The result was a recovery across equity markets, with U.S. stocks rebounding sharply.

| Total returns ending 06/30/2026 |

Q2 ‘26 |

1 Year |

3 Years |

5 Years |

10 Years |

20 Years |

| S&P 500 Index |

15.2% |

22.3% |

20.6% |

13.4% |

15.5% |

11.4% |

| Russell 2000 Index |

21.5% |

40.8% |

18.6% |

7.0% |

11.6% |

8.9% |

| MSCI EAFE Index |

11.1% |

20.8% |

17.0% |

9.6% |

10.2% |

6.0% |

| MSCI Emerging Markets Index |

24.1% |

44.2% |

23.6% |

7.7% |

10.5% |

7.1% |

| S&P Global REIT Index |

10.8% |

15.4% |

10.1% |

2.9% |

3.8% |

4.3% |

| Bloomberg U.S. Aggregate Bond Index |

0.7% |

3.8% |

4.2% |

0.1% |

1.5% |

3.3% |

| Bloomberg Municipal Bond Index 1-10 Years |

1.3% |

4.5% |

3.4% |

1.4% |

1.9% |

3.1% |

| Bloomberg U.S. Corp High Yield Bond Index |

2.5% |

5.9% |

8.9% |

4.2% |

5.8% |

6.7% |

The returns shown are annualized returns for benchmark indices. Investors cannot invest directly in an index. Unmanaged indices do not reflect management fees or transaction costs. Past performance is not a guarantee of future results. Source: Ycharts. See full disclosures.

One of the most encouraging developments year-to-date has been the broadening of market leadership. International developed markets have outperformed the U.S. for much of the year, supported by more attractive valuations and improving earnings expectations. Smaller companies also regained momentum as investors became more confident that economic growth would remain positive, with the Russell 2000 Small Cap Index delivering its strongest first half since 1991.1 This broader participation may be viewed as a positive development of for long-term investors because it can reduce dependence on a small group of companies to drive portfolio returns.

Fixed income also made a meaningful contribution to diversified portfolios. Higher starting yields continue to provide attractive income, while high-quality investment-grade bonds and municipal bonds generated solid returns and once again demonstrated their value as potential portfolio stabilizers. Investment-grade corporate bonds benefited from healthy corporate fundamentals, while Treasury securities continued to provide important diversification despite ongoing interest-rate volatility.

For long-term investors, the first half of the year reinforces an important lesson: the potential benefits of diversification. Leadership shifted from quarter to quarter, with different regions, market capitalizations, investment styles, and asset classes taking turns leading performance. Rather than attempting to predict these rotations, maintaining a globally diversified portfolio allows investors to participate wherever opportunities emerge while helping reduce the risks associated with concentrating in any single market or investment style. That disciplined approach may help investors pursue long-term wealth accumulation.

The Economy

Economic growth continues to hold up, and inflation pressures could ease if oil prices continue to decline. U.S. real GDP grew at a 2.1% annualized rate in the first quarter, up from 0.5% in Q4 20252.

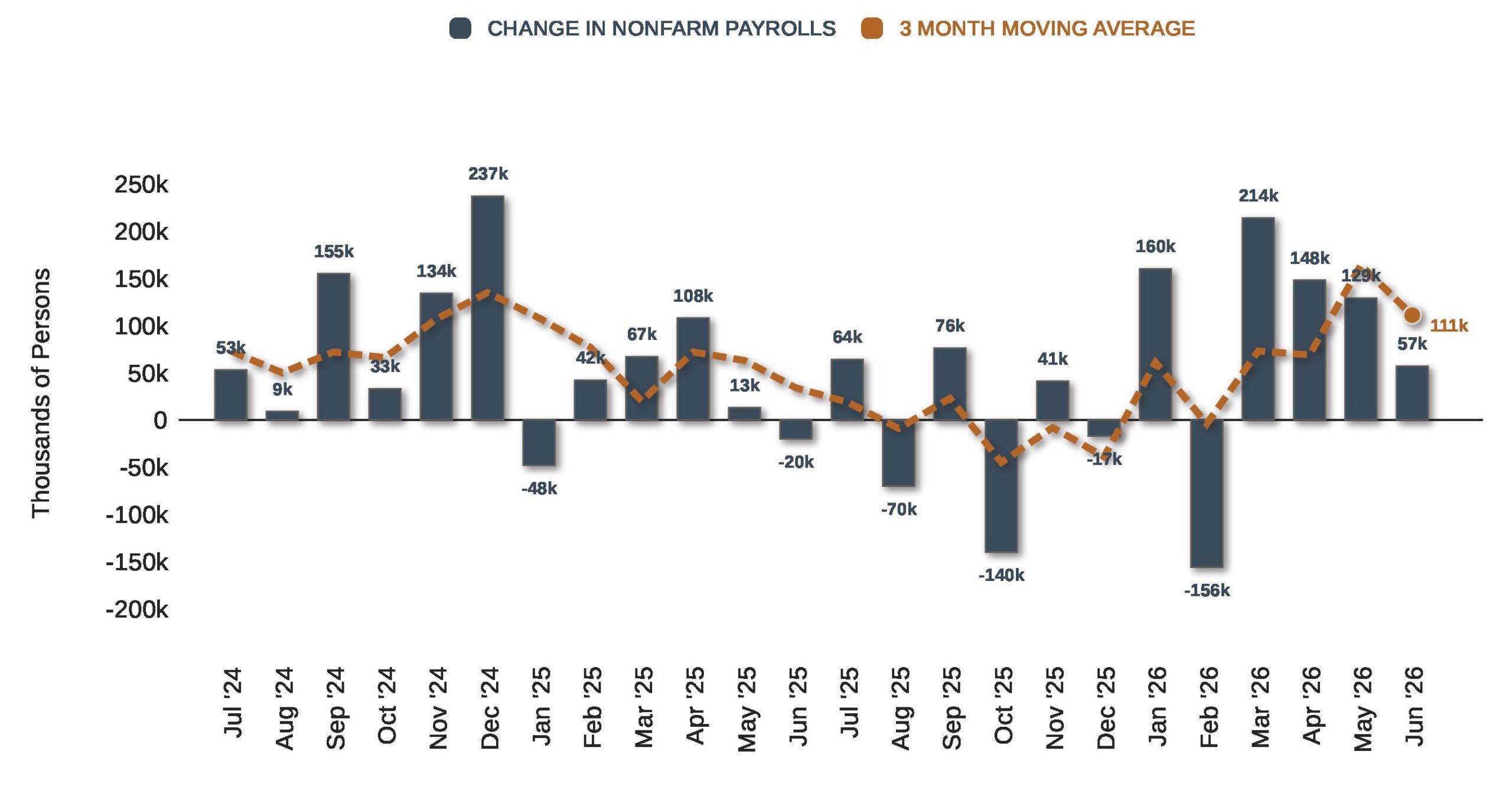

A Look at Monthly Job Growth

Monthly Change in Nonfarm Payrolls with 3-month Moving Average, Past 2 Years

Source: © Exhibit A, U.S. Bureau of Labor Statistics via FRED | Latest: 2026-06-01

This slide is for informational and illustrative purposes only. The data provided is believed to be accurate, but there is no guarantee of its accuracy, completeness, or timeliness. This is not a recommendation or offer of any financial product. Past performance is not indicative of future results, and investors should consider their own objectives and risk tolerance. Indices, if presented, do not include fees, are unmanaged, and not available for direct investment. Definitions & Methodology: Nonfarm Payrolls measures the total number of paid workers in the U.S. economy, excluding farmworkers, government employees, and nonprofit workers. It is a major labor market indicator. The chart shows the monthly change in nonfarm payrolls with a 3-month moving average. A 3-Month Moving Average smooths out short-term fluctuations by averaging data from the past three months. It helps show trends more clearly by reducing month-to-month volatility. As new data comes in, the average updates by replacing the oldest month with the newest.

Halfway through the year, the labor market appears relatively stable compared with the uncertainty of 2025, supporting the case for continued, albeit moderate, economic expansion.3 Through the first half of 2026, the economy added approximately 99,000 jobs per month, a sharp improvement from the average monthly loss of 8,000 jobs during the second half of 2025. Continued consumer spending, easing policy uncertainty, supportive tax policy, and robust investment in AI infrastructure may have helped sustain hiring, particularly in construction and other cyclical sectors.

Twelve months ago, companies were facing steep new tariffs, and now some companies are receiving tariff refunds while tax cuts may be providing support to consumers and businesses. These developments could help support corporate earnings and financial markets over the remainder of the year.

The Federal Reserve

One of the more significant developments for investors is the change in leadership at the Federal Reserve. New chair Kevin Warsh has already signaled that while the Fed’s dual mandate of price stability and maximum employment remains unchanged, how the Fed communicates and implements policy is likely to look very different.4 For students of economic history, this may look similar in some respects to the Greenspan era.

Alan Greenspan, who recently passed away at the age of 100, presided over one of the longest periods of economic growth at that time, much of it stemming from the nascent technology revolution that began in the mid-1990s. During his tenure, tech productivity gains helped the economy to grow without igniting inflation, which in turn permitted the Fed to keep interest rates relatively low. Warsh faces a potentially similar situation, with AI expected some analysts to create even greater productivity efficiencies that could support continued economic growth.

Let’s not forget that all was not wine and roses during Greenspan’s era: the 1987 stock market crash, the 1998 failure of Long-Term Capital Management, the bursting of the dot-com bubble, and several major corporate scandals. When he did speak, Alan Greenspan was ambiguous and opaque, saying much but imparting little.

There are stark differences between then and now. During the 1990s, the budget moved from a steep deficit to a surplus, political polarization was markedly lower, and the end of the Cold War led to global economic expansion. Greenspan benefited from globalization, favorable demographics, and decades of steadily declining inflation and interest rates that helped the U.S. economy grow to unprecedented heights.

Chair Warsh faces a very different backdrop today. The Fed is contending with historically high federal deficits, fractured political parties, inflation uncertainty, and multiple geopolitical events occurring simultaneously. The flow of information moves markets almost instantly.

Warsh appears to be embracing his inner Greenspan by sharply curtailing the issuance of forward guidance and seems to be following a more rules-based approach to Fed operations and strategies. Like Greenspan, Warsh appears comfortable with the idea that low inflation, strong economic growth, and low unemployment can coexist in the big U.S. economic tent. Whether Warsh’s tenure will also be defined by historic economic growth remains to be seen.

What We’re Watching Over the Next 6–9 Months

Markets have rewarded patient investors, but we expect volatility to remain elevated as we enter the second half of the year. Rather than trying to predict every market move, we’re focused on the factors most likely to influence long-term portfolio returns.

Earnings growth must continue to support valuations

The market’s recovery has been driven primarily by stronger corporate earnings and optimism surrounding artificial intelligence and productivity gains. While valuations remain above historical averages, particularly among the largest technology companies, they may be justified if earnings continue to grow. Over the next several quarters, we’ll be watching whether companies can deliver on those expectations. Healthy earnings growth would likely support further market gains, while disappointments could lead to periods of increased volatility.

Inflation is making headlines but is expected to subside

Inflation expectations appear to have peaked in March, boosted by a spike in oil prices during the Iran conflict. Gold and oil prices have retreated since March as geopolitical tensions have eased.5 More stable global economic conditions could also mean a stronger dollar, reinforcing lower inflation.

Some think higher inflation is causing interest rates to climb. While interest rates have moved higher, the increase appears to have been driven primarily by rising real yields, not worsening inflation. At the same time, manufacturing activity is strengthening in the U.S. and Europe, and the labor market remains stable.6

Still, inflation remains above the Federal Reserve’s long-term target. Investors are increasingly focused on the timing and pace of future interest rate moves, including the potential for increases. Progress is unlikely to be perfectly smooth. We expect markets to react to each inflation report and Fed meeting, creating short-term swings that long-term investors should view as normal rather than alarming.

Together, these trends support our view that inflation should continue to moderate as economic growth gradually improves.

Broader market leadership is a constructive development

One of the most encouraging trends this year has been the expansion of market leadership beyond a handful of mega-cap technology companies. International stocks, smaller companies, value-oriented investments, and many areas of fixed income have all contributed meaningfully to diversified portfolio returns. Broader participation may create a more diversified investment environment than one driven by a single sector or investment style. Diversification remains one of the few strategies investors can control. Rather than trying to guess which asset class will lead next, maintaining exposure across global markets, company sizes, investment styles, and high-quality fixed income positions portfolios to benefit regardless of where opportunities emerge.

Interest rates should remain steady: a new Fed Chair, not a new mandate

While we believe the most likely outcome over the next 6-9 months is that the Fed keeps rates unchanged for an extended period, the probability of a rate increase may be higher today than it was just a few months ago. However, we shouldn’t presume that the Fed will quickly shift policy, or signal shifts based on just a few data points.

We expect to see a more disciplined, data-dependent Federal Reserve that places restoring and maintaining price stability ahead of smoothing short-term market fluctuations. This could ultimately support long-term economic growth and investment returns.

Your Spoonful of Sugar

As we turn our focus to the second half of the year, it’s worth remembering that while the current environment seems uniquely chaotic, there are still reasons to remain optimistic. Every era contends with its own concoction of challenges and struggles. Even a summertime drive-in confection like “Mary Poppins” confronts Edwardian themes of class and hierarchy, bureaucracy and capitalism, social stability and voting rights that could be plucked straight out of today’s headlines. But the film also reminds us that joy and human connection give our lives meaning, underlining the importance of enjoying family, friends, and adventures this summer. And of course, Mr. Banks reminds us that tuppence invested wisely may compound. Some things never change.

1 https://www.cnbc.com/2026/06/30/small-cap-stocks-enjoy-best-first-half-since-1991-as-ai-trade-expands.html

2 https://www.bea.gov/data/gdp/gross-domestic-product

3 https://www.bls.gov/news.release/archives/empsit_02112026.htm

4 https://www.federalreserve.gov/aboutthefed/fedexplained/monetary-policy.htm

5 https://fred.stlouisfed.org/series/WTISPLC

6 https://www.ismworld.org/globalassets/pub/research-and-surveys/rob/pmi/hotdm202606pmi.pdf

Definitions

Nonfarm Payrolls measures the total number of paid workers in the U.S. economy, excluding farm workers, government employees, and nonprofit workers. It is a major labor market indicator.

A 3-Month Moving Average smooths out short-term fluctuations by averaging data from the past three months. It helps show trends more clearly by reducing month-to-month volatility. As new data comes in, the average updates by replacing the oldest month with the newest.

Exhibit A Disclosures

Copyright © 2026 Exhibit A for Advice LLC. All rights reserved. The materials provided here are based on information from sources believed to be reliable, but no guarantee is made regarding their completeness or accuracy. Exhibit A for Advice LLC does not represent or warrant the fairness, correctness, or accuracy of any information or opinions shared. The content, including charts and analyses, may change without notice. The materials provided are not intended to address the specific financial circumstances or investment goals of any individual and should not be interpreted as an offer or solicitation to buy or sell any securities or other financial instruments. Past performance is not indicative of future results, and no predictions or forecasts should be construed as recommendations. References to company fundamentals, earnings, or market predictions are purely for informational purposes and are not to be construed as investment advice or endorsement to buy, sell, or hold securities. Exhibit A for Advice LLC shall not be held liable for any losses or damages, direct or indirect, arising from the use of this material, including any investment decisions based on the information provided. Users are strongly advised to verify the accuracy of the data independently before making any financial or investment decisions. The data provided by Standard & Poor’s (©2026) and FactSet Research Systems Inc. (© 2026) is used under license and remains the property of those organizations. The use of third-party data from Standard & Poor’s and FactSet Research Systems Inc. does not imply any endorsement or affiliation with Exhibit A for Advice LLC. Data sourced from the Federal Reserve Economic Data (FRED) is publicly available and is used here for informational purposes. Note: The materials presented are created by Exhibit A for Advice LLC and may be branded with the advisor’s logo for presentation purposes. However, Exhibit A for Advice LLC retains all intellectual property rights to the content, and the advisor is licensed to use this material solely for client education and advisory purposes. Unauthorized use, reproduction, or distribution of these materials is prohibited and constitutes an infringement of Exhibit A for Advice LLC’s intellectual property rights. The content, images, and reports created and displayed by Exhibit A for Advice LLC are proprietary intellectual property. Any unauthorized use or reproduction of Exhibit A for Advice LLC’s materials will be considered a violation of copyright and other intellectual property rights. Exhibit A for Advice LLC reserves the right to take legal action, including both civil and criminal remedies, for any infringement of these rights. Additionally, Exhibit A for Advice LLC retains the right to monitor the use of its materials and services through electronic tracking or other methods, as allowed by law. These terms and conditions shall be governed by and construed in accordance with the laws of New York. Any disputes shall be resolved in the appropriate courts located in New York. Exhibit A for Advice LLC respects your privacy and adheres to applicable privacy laws. For more information, please refer to our Privacy Policy available on our website. Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may “will “should ” “expect “anticipate “project “estimate “intend “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Investment Commentary: Q2 2026

George Padula, CFA®, CFP®

Wealth Manager, Principal

When uncertainty dominates the conversation, maintaining perspective is often the most valuable investment strategy of all.

When my daughters were young, they loved going to the drive-in movies during the summer. There was something special about being outdoors under the stars, with crickets chirping, the radio crackling, and the scents of popcorn, hot dogs, and fried dough all around. They would create a cozy bed out of what seemed to be every blanket in the house. Suddenly, the biggest screen a child could imagine lit with color, lights, and movement, the ensuing magic capturing their rapt attention.

Those summer evenings at the drive-in came to mind recently when I was asked how I would describe today’s investment markets. Oddly enough, I thought of the movie “Mary Poppins.” Don’t ask me why, but my gut reaction was to say that today’s markets are supercalifragilisticexpialidocious. If you remember “Mary Poppins,” you are familiar with that word. Even though the sound of it is something quite atrocious, it is as good a descriptor as I can think of to summarize the current economic situation.

Like the infamous word, not everything meaningful is easy to explain. Investing works the same way. Short-term swings are noisy, emotional, and can be unsettling. We are constantly navigating so many uncertainties: interest rates, geopolitics, oil, inflation, and artificial intelligence, to name a few. However, while these uncertainties may fuel short-term volatility, they rarely change the long-term drivers of wealth creation.

Supercalifragilisticexpialidocious stands out because it makes little sense; long-term investing stands out because it does. Investing isn’t about finding magic. Rather, it’s about adhering to key principles. Disciplined, patient investors who stay focused on quality, innovation, earnings growth, diversification, and the power of compounding are typically rewarded over time.

When uncertainty dominates the conversation, maintaining perspective is often the most valuable investment strategy of all.

Markets

The first half of the year was a good reminder that markets rarely move in a straight line. The first quarter was dominated by geopolitical tensions, tariff concerns, sticky inflation, and talk of Federal Reserve rate cuts. That uncertainty weighed most heavily on U.S. large-cap growth stocks, while value stocks and smaller companies held up relatively better. International markets were mixed, and bond returns were modest as interest rates moved higher.

The second quarter told a very different story. Investor sentiment appeared to improve as corporate earnings remained resilient, the U.S. economy continued to expand, and fears of a meaningful economic slowdown eased. Markets focused on healthy earnings growth and the longer-term benefits that artificial intelligence and business investment may provide. The result was a recovery across equity markets, with U.S. stocks rebounding sharply.

The returns shown are annualized returns for benchmark indices. Investors cannot invest directly in an index. Unmanaged indices do not reflect management fees or transaction costs. Past performance is not a guarantee of future results. Source: Ycharts. See full disclosures.

One of the most encouraging developments year-to-date has been the broadening of market leadership. International developed markets have outperformed the U.S. for much of the year, supported by more attractive valuations and improving earnings expectations. Smaller companies also regained momentum as investors became more confident that economic growth would remain positive, with the Russell 2000 Small Cap Index delivering its strongest first half since 1991.1 This broader participation may be viewed as a positive development of for long-term investors because it can reduce dependence on a small group of companies to drive portfolio returns.

Fixed income also made a meaningful contribution to diversified portfolios. Higher starting yields continue to provide attractive income, while high-quality investment-grade bonds and municipal bonds generated solid returns and once again demonstrated their value as potential portfolio stabilizers. Investment-grade corporate bonds benefited from healthy corporate fundamentals, while Treasury securities continued to provide important diversification despite ongoing interest-rate volatility.

For long-term investors, the first half of the year reinforces an important lesson: the potential benefits of diversification. Leadership shifted from quarter to quarter, with different regions, market capitalizations, investment styles, and asset classes taking turns leading performance. Rather than attempting to predict these rotations, maintaining a globally diversified portfolio allows investors to participate wherever opportunities emerge while helping reduce the risks associated with concentrating in any single market or investment style. That disciplined approach may help investors pursue long-term wealth accumulation.

The Economy

Economic growth continues to hold up, and inflation pressures could ease if oil prices continue to decline. U.S. real GDP grew at a 2.1% annualized rate in the first quarter, up from 0.5% in Q4 20252.

A Look at Monthly Job Growth

Monthly Change in Nonfarm Payrolls with 3-month Moving Average, Past 2 Years

Source: © Exhibit A, U.S. Bureau of Labor Statistics via FRED | Latest: 2026-06-01

This slide is for informational and illustrative purposes only. The data provided is believed to be accurate, but there is no guarantee of its accuracy, completeness, or timeliness. This is not a recommendation or offer of any financial product. Past performance is not indicative of future results, and investors should consider their own objectives and risk tolerance. Indices, if presented, do not include fees, are unmanaged, and not available for direct investment. Definitions & Methodology: Nonfarm Payrolls measures the total number of paid workers in the U.S. economy, excluding farmworkers, government employees, and nonprofit workers. It is a major labor market indicator. The chart shows the monthly change in nonfarm payrolls with a 3-month moving average. A 3-Month Moving Average smooths out short-term fluctuations by averaging data from the past three months. It helps show trends more clearly by reducing month-to-month volatility. As new data comes in, the average updates by replacing the oldest month with the newest.

Halfway through the year, the labor market appears relatively stable compared with the uncertainty of 2025, supporting the case for continued, albeit moderate, economic expansion.3 Through the first half of 2026, the economy added approximately 99,000 jobs per month, a sharp improvement from the average monthly loss of 8,000 jobs during the second half of 2025. Continued consumer spending, easing policy uncertainty, supportive tax policy, and robust investment in AI infrastructure may have helped sustain hiring, particularly in construction and other cyclical sectors.

Twelve months ago, companies were facing steep new tariffs, and now some companies are receiving tariff refunds while tax cuts may be providing support to consumers and businesses. These developments could help support corporate earnings and financial markets over the remainder of the year.

The Federal Reserve

One of the more significant developments for investors is the change in leadership at the Federal Reserve. New chair Kevin Warsh has already signaled that while the Fed’s dual mandate of price stability and maximum employment remains unchanged, how the Fed communicates and implements policy is likely to look very different.4 For students of economic history, this may look similar in some respects to the Greenspan era.

Alan Greenspan, who recently passed away at the age of 100, presided over one of the longest periods of economic growth at that time, much of it stemming from the nascent technology revolution that began in the mid-1990s. During his tenure, tech productivity gains helped the economy to grow without igniting inflation, which in turn permitted the Fed to keep interest rates relatively low. Warsh faces a potentially similar situation, with AI expected some analysts to create even greater productivity efficiencies that could support continued economic growth.

Let’s not forget that all was not wine and roses during Greenspan’s era: the 1987 stock market crash, the 1998 failure of Long-Term Capital Management, the bursting of the dot-com bubble, and several major corporate scandals. When he did speak, Alan Greenspan was ambiguous and opaque, saying much but imparting little.

There are stark differences between then and now. During the 1990s, the budget moved from a steep deficit to a surplus, political polarization was markedly lower, and the end of the Cold War led to global economic expansion. Greenspan benefited from globalization, favorable demographics, and decades of steadily declining inflation and interest rates that helped the U.S. economy grow to unprecedented heights.

Chair Warsh faces a very different backdrop today. The Fed is contending with historically high federal deficits, fractured political parties, inflation uncertainty, and multiple geopolitical events occurring simultaneously. The flow of information moves markets almost instantly.

Warsh appears to be embracing his inner Greenspan by sharply curtailing the issuance of forward guidance and seems to be following a more rules-based approach to Fed operations and strategies. Like Greenspan, Warsh appears comfortable with the idea that low inflation, strong economic growth, and low unemployment can coexist in the big U.S. economic tent. Whether Warsh’s tenure will also be defined by historic economic growth remains to be seen.

What We’re Watching Over the Next 6–9 Months

Markets have rewarded patient investors, but we expect volatility to remain elevated as we enter the second half of the year. Rather than trying to predict every market move, we’re focused on the factors most likely to influence long-term portfolio returns.

Earnings growth must continue to support valuations

The market’s recovery has been driven primarily by stronger corporate earnings and optimism surrounding artificial intelligence and productivity gains. While valuations remain above historical averages, particularly among the largest technology companies, they may be justified if earnings continue to grow. Over the next several quarters, we’ll be watching whether companies can deliver on those expectations. Healthy earnings growth would likely support further market gains, while disappointments could lead to periods of increased volatility.

Inflation is making headlines but is expected to subside

Inflation expectations appear to have peaked in March, boosted by a spike in oil prices during the Iran conflict. Gold and oil prices have retreated since March as geopolitical tensions have eased.5 More stable global economic conditions could also mean a stronger dollar, reinforcing lower inflation.

Some think higher inflation is causing interest rates to climb. While interest rates have moved higher, the increase appears to have been driven primarily by rising real yields, not worsening inflation. At the same time, manufacturing activity is strengthening in the U.S. and Europe, and the labor market remains stable.6

Still, inflation remains above the Federal Reserve’s long-term target. Investors are increasingly focused on the timing and pace of future interest rate moves, including the potential for increases. Progress is unlikely to be perfectly smooth. We expect markets to react to each inflation report and Fed meeting, creating short-term swings that long-term investors should view as normal rather than alarming.

Together, these trends support our view that inflation should continue to moderate as economic growth gradually improves.

Broader market leadership is a constructive development

One of the most encouraging trends this year has been the expansion of market leadership beyond a handful of mega-cap technology companies. International stocks, smaller companies, value-oriented investments, and many areas of fixed income have all contributed meaningfully to diversified portfolio returns. Broader participation may create a more diversified investment environment than one driven by a single sector or investment style. Diversification remains one of the few strategies investors can control. Rather than trying to guess which asset class will lead next, maintaining exposure across global markets, company sizes, investment styles, and high-quality fixed income positions portfolios to benefit regardless of where opportunities emerge.

Interest rates should remain steady: a new Fed Chair, not a new mandate

While we believe the most likely outcome over the next 6-9 months is that the Fed keeps rates unchanged for an extended period, the probability of a rate increase may be higher today than it was just a few months ago. However, we shouldn’t presume that the Fed will quickly shift policy, or signal shifts based on just a few data points.

We expect to see a more disciplined, data-dependent Federal Reserve that places restoring and maintaining price stability ahead of smoothing short-term market fluctuations. This could ultimately support long-term economic growth and investment returns.

Your Spoonful of Sugar

As we turn our focus to the second half of the year, it’s worth remembering that while the current environment seems uniquely chaotic, there are still reasons to remain optimistic. Every era contends with its own concoction of challenges and struggles. Even a summertime drive-in confection like “Mary Poppins” confronts Edwardian themes of class and hierarchy, bureaucracy and capitalism, social stability and voting rights that could be plucked straight out of today’s headlines. But the film also reminds us that joy and human connection give our lives meaning, underlining the importance of enjoying family, friends, and adventures this summer. And of course, Mr. Banks reminds us that tuppence invested wisely may compound. Some things never change.

1 https://www.cnbc.com/2026/06/30/small-cap-stocks-enjoy-best-first-half-since-1991-as-ai-trade-expands.html

2 https://www.bea.gov/data/gdp/gross-domestic-product

3 https://www.bls.gov/news.release/archives/empsit_02112026.htm

4 https://www.federalreserve.gov/aboutthefed/fedexplained/monetary-policy.htm

5 https://fred.stlouisfed.org/series/WTISPLC

6 https://www.ismworld.org/globalassets/pub/research-and-surveys/rob/pmi/hotdm202606pmi.pdf

Definitions

Nonfarm Payrolls measures the total number of paid workers in the U.S. economy, excluding farm workers, government employees, and nonprofit workers. It is a major labor market indicator.

A 3-Month Moving Average smooths out short-term fluctuations by averaging data from the past three months. It helps show trends more clearly by reducing month-to-month volatility. As new data comes in, the average updates by replacing the oldest month with the newest.

Exhibit A Disclosures

Copyright © 2026 Exhibit A for Advice LLC. All rights reserved. The materials provided here are based on information from sources believed to be reliable, but no guarantee is made regarding their completeness or accuracy. Exhibit A for Advice LLC does not represent or warrant the fairness, correctness, or accuracy of any information or opinions shared. The content, including charts and analyses, may change without notice. The materials provided are not intended to address the specific financial circumstances or investment goals of any individual and should not be interpreted as an offer or solicitation to buy or sell any securities or other financial instruments. Past performance is not indicative of future results, and no predictions or forecasts should be construed as recommendations. References to company fundamentals, earnings, or market predictions are purely for informational purposes and are not to be construed as investment advice or endorsement to buy, sell, or hold securities. Exhibit A for Advice LLC shall not be held liable for any losses or damages, direct or indirect, arising from the use of this material, including any investment decisions based on the information provided. Users are strongly advised to verify the accuracy of the data independently before making any financial or investment decisions. The data provided by Standard & Poor’s (©2026) and FactSet Research Systems Inc. (© 2026) is used under license and remains the property of those organizations. The use of third-party data from Standard & Poor’s and FactSet Research Systems Inc. does not imply any endorsement or affiliation with Exhibit A for Advice LLC. Data sourced from the Federal Reserve Economic Data (FRED) is publicly available and is used here for informational purposes. Note: The materials presented are created by Exhibit A for Advice LLC and may be branded with the advisor’s logo for presentation purposes. However, Exhibit A for Advice LLC retains all intellectual property rights to the content, and the advisor is licensed to use this material solely for client education and advisory purposes. Unauthorized use, reproduction, or distribution of these materials is prohibited and constitutes an infringement of Exhibit A for Advice LLC’s intellectual property rights. The content, images, and reports created and displayed by Exhibit A for Advice LLC are proprietary intellectual property. Any unauthorized use or reproduction of Exhibit A for Advice LLC’s materials will be considered a violation of copyright and other intellectual property rights. Exhibit A for Advice LLC reserves the right to take legal action, including both civil and criminal remedies, for any infringement of these rights. Additionally, Exhibit A for Advice LLC retains the right to monitor the use of its materials and services through electronic tracking or other methods, as allowed by law. These terms and conditions shall be governed by and construed in accordance with the laws of New York. Any disputes shall be resolved in the appropriate courts located in New York. Exhibit A for Advice LLC respects your privacy and adheres to applicable privacy laws. For more information, please refer to our Privacy Policy available on our website. Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may “will “should ” “expect “anticipate “project “estimate “intend “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Follow us on social:

Related Articles:

Talk to an experienced financial planner

Related Articles:

Modera Wealth Management, LLC (Modera) is an SEC-registered investment adviser. SEC registration does not imply any level of skill or training. For information pertaining to our registration status, the fees we charge including how we are compensated and by whom, additional costs that may be incurred, our conflicts of interest, any disclosed disciplinary events of the Firm or its personnel, and the types of services we offer, please contact us directly or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov) to obtain a copy of our disclosure statement, Form ADV Part 2A, and ADV Part 3/Form CRS. In addition, our Privacy Notice outlines how we handle your non-public personal information. Please read these documents carefully before you make a decision to hire Modera, invest or send money.

This material is limited to the dissemination of general information about Modera’s investment advisory and financial planning services that is not suitable for everyone. Nothing herein should be interpreted or construed as investment advice nor as legal, tax or accounting advice nor as personalized financial planning, tax planning or wealth management advice. For legal, tax and accounting-related matters, we recommend you seek the advice of a qualified attorney or accountant. This material is not a substitute for personalized investment or financial planning from Modera. There is no guarantee that the views and opinions expressed herein will come to pass, and the information herein should not be considered a solicitation to engage in a particular investment or financial planning strategy. The statements and opinions expressed in this material are relevant as of the date of publication and are subject to change without notice based on changes in the law and other conditions.

Investing in the markets involves gains and losses and may not be suitable for all investors. Information herein is subject to change without notice and should not be considered a solicitation to buy or sell any security or to engage in a particular investment or financial planning strategy. Individual client asset allocations and investment strategies differ based on varying degrees of diversification and other factors. Diversification does not guarantee a profit or guarantee against a loss.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.