A good friend and I frequently text about the Red Sox’s chances for the upcoming season. He typically takes a more optimistic view, while I am more realistic about their chances. Either way, the team gives us ample opportunity to cheer the highs and lament the lows.

We both agree, though, that Ted Williams was the greatest hitter of all time. Yes, you Yankees, Giants, Dodgers, and Cardinals fans will put in plugs for DiMaggio, Bonds, Piazza, and Musial. I get it. All are great. But they were not Ted Williams. First published in 1971, his book, “The Science of Hitting”, is still a gem. Williams was disciplined, educated, patient, and focused on the fundamentals. His secret was as simple as “getting a good pitch to hit.” Undisciplined hitters become impatient, and overconfident, impulsively chasing bad pitches, making poor decision after poor decision.

For Ted Williams, a good long-term decision process was the key starting point. It is a lot like investing.

The fundamentals: valuation, diversification, discipline, and risk management are necessary. Good investing requires deep self-awareness, an understanding of constraints, and knowledge of the game being played. These conditions are when the “good investing pitches” start to appear.

The war in Iran and the surrounding regional tensions have made this an undeniably difficult period. But if we are true investors, with a sound long-term process, this conflict alone may not warrant stopping or dramatically changing a long‑term investment plan. Now more than ever, having an investment process matters. Knowing how and why to make investment decisions is as important as the outcomes. Being patient and not chasing bad investments may help support better long‑term outcomes.

Last quarter, I wrote that optimism and skepticism can be both held at the same time. Nothing in the last three months has changed that.

As we head into the commentary, there are really three themes of focus: interest rates, economic growth and market volatility.

Geopolitics and the oil shock: what is different today?

The first quarter reminded investors how quickly markets can flip from optimism to uncertainty. After a strong finish to 2025, Q1 2026 was dominated by geopolitics, specifically the escalating conflict involving Iran, and the resulting shock to global energy markets. While uncomfortable, these events also reinforced why disciplined portfolio construction and long-term focus remain essential.

The dominant narrative of the quarter was the conflict within Iran and its implications for global energy supply. Disruptions and threats around the Strait of Hormuz, a critical artery for roughly one‑fifth of the world’s oil supply, sent crude prices sharply higher with Brent oil surging above $100 per barrel.

These price spikes flowed quickly through the economy, reigniting inflation concerns.

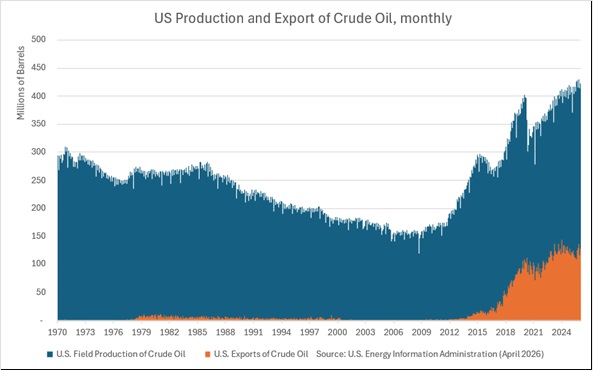

Here in the U.S., the long-term impact from higher prices will likely be muted. According to data from the U.S. Energy Information Administration, petroleum production and exports are far higher now than they ever have been with daily production up 170% vs. 1980 and 40% higher than 1970. At the same time, U.S. crude oil exports have gone from almost nothing twenty years ago to approximately 1.5 billion barrels per year. While this energy transformation gives the U.S. more flexibility, it doesn’t mean that gasoline prices and heating costs won’t increase. Rather, the rate of increase may likely be less than they would have been otherwise.

From an investment perspective, markets can respond in various ways to supply shocks, and energy‑related inflation may moderate as conditions stabilize.

Markets in Q1 were mixed

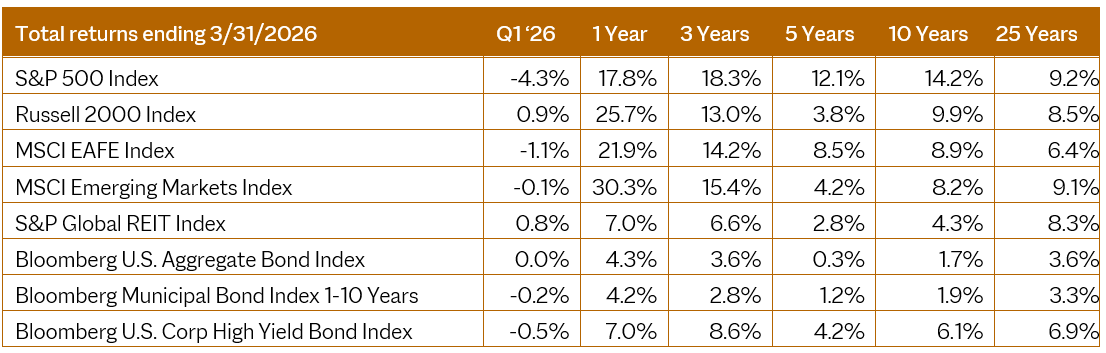

Looking at the chart below, we see that equity markets started out strong and then pulled back sharply in March with the conflict in Iran. The large cap, tech-heavy S&P 500 declined approximately 4% for the quarter. However, not all markets declined. The Russell 2000 small cap index gained 0.9% and global real estate was up 0.8%. Bonds were mixed as interest rates were both up and down.

International equities were relatively resilient despite the global uncertainty. Over the last 12 months, developed international and emerging market indices outperformed U.S. indices.

Bonds, meanwhile, were challenged as inflation risks pushed yields higher, leaving broad U.S. bond benchmarks flat to slightly negative year‑to‑date.

The returns shown are annualized returns for benchmark indices. Investors cannot invest directly in an index. Unmanaged indices do not reflect management fees or transaction costs. Past performance is not a guarantee of future results. Source: Ycharts. See full disclosures.

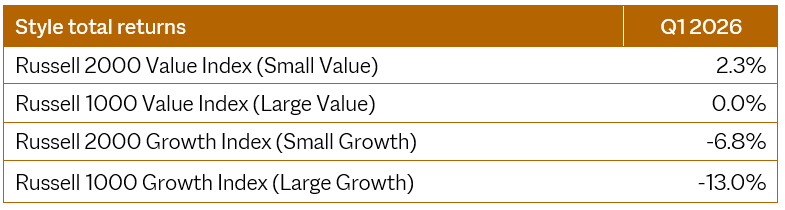

Digging deeper, there was a large difference in styles, with the Russell 2000 Value Index (Small Value) outperforming the Russell 1000 Growth Index (Large Growth) as indicated below. This tilt to value began in 2025 with worries about an AI bubble and the technology’s effect on software companies and has continued as the war in Iran boosts value-oriented stocks in energy and defense industries.

Source: Ycharts

Taken together, this all highlights the role of diversification during a time of market stress.

What’s on investors’ minds

Given all this movement across styles, sectors, and global events, it’s natural to wonder what it all means for your portfolio and what questions matter most right now. And if you’re asking yourself some of the same questions we’re hearing from investors, you’re not alone.

These ups and downs and volatility seem out of the ordinary. Should I be worried?

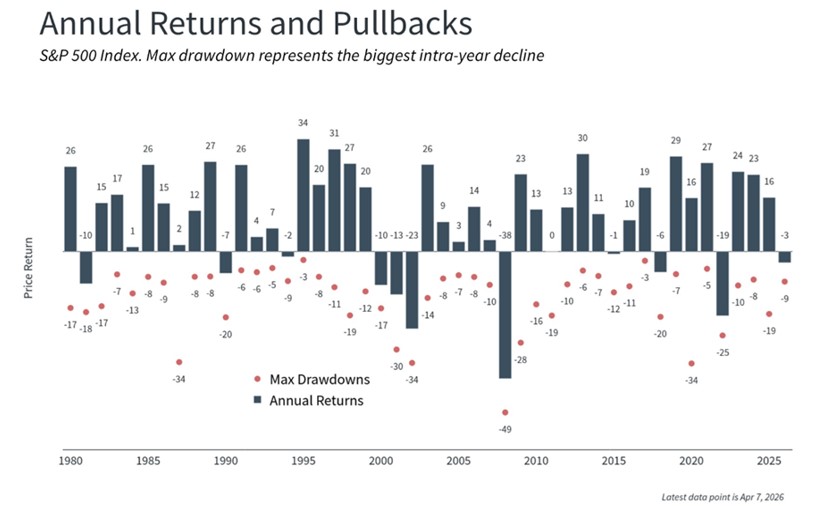

Market ups and downs are a feature of investing, not a flaw. From a longer‑term perspective, these recent market moves are well within historical norms. Pullbacks occur regularly, even in strong market years, and naturally occur amid changing information and sentiment. This chart shows the performance of the S&P 500 (bars) and the largest intra-year decline (dots) each year. The average year sees a stock market drop of -13.5%. However, most years still end in positive territory (see chart below). Volatility is a normal part of investing and investors are often rewarded for staying disciplined through short-term volatility.

Source: Clearnomics

How fearful should we be of a recession? With oil prices increasing, jobs all over the place, and both inflation and rates rising, a recession seems inevitable.

Rising oil prices, mixed job signals, and higher inflation and rates can create a convincing “perfect storm.” But what feels inevitable isn’t always what’s most likely. Recessions are not triggered by headlines.

While the chance of an economic slowdown or mild recession is elevated, the likelihood of a deep, prolonged downturn still appears relatively low. While the above pressure points are real, we are not seeing them at critical levels, and there are multiple relief valves still in place.

The labor market remains strong, without the broad job losses that typically precede recessions. Consumers and businesses are still in solid financial shape, unlike prior downturns. Even with the possibility of higher energy prices, inflation has moderated from its peak, reducing the need for further aggressive tightening.

Our focus isn’t about predicting a recession, but it is about being prepared for one. Going back to our disciplined process: Stay diversified, emphasize quality and resilience, maintain liquidity aligned with your needs. It’s natural to feel concerned, but this is a time for discipline, not reaction. Historically, markets tend to recover before the data improves, so reacting emotionally may be costly.

The economy seems so confusing. How concerned should I be?

It does feel confusing right now, because the signals are mixed. The U.S. economy entered 2026 on solid footing, but expectations are tempered. Consumer spending remains resilient, though hiring may be slowing and the unemployment rate has drifted modestly higher. Inflation remains an uncertain challenge and the Fed signaled a cautious, data‑dependent approach.

In our view, while the picture is more complex than usual, on the whole, it’s not one that currently points to a severe or systemic breakdown.

Interest rates: With so much uncertainty, why isn’t the Federal Reserve cutting rates?

That’s a very fair question, and it gets to the heart of what the Federal Reserve is managing right now. At the start of the year, consensus estimates had the Fed cutting rates a few times in 2026. However they are now in a policy pause, not a policy shift.

The Iranian conflict has clearly increased inflation risks over the short term, and the Fed is signaling a cautious approach. At their March meeting, the Fed took any 2026 rate cuts off the table but noted the longer-term trend of decreasing interest rates remains. It is likely that interest rates will remain unchanged through the end of 2026. Essentially, the two 2026 cuts may be pushed into next year starting with the Fed’s meeting in June 2027. This pause gives the Fed room to maneuver if economic conditions sharply deteriorate.

While higher‑for‑longer rates can create short‑term headwinds for bonds, yields today offer far more income than in prior years, improving long‑term return potential for diversified fixed income.

Key Takeaways for Portfolios

We mentioned at the start that a disciplined process is crucial as we navigate the remainder of 2026. Staying focused, grounded, and aligned with long‑term goals helps put short‑term volatility into context.

- We are monitoring risks but not overreacting to them.

- It’s better to stay attentive than anxious.

- Geopolitical conflicts often increase volatility, but their long‑term impact on diversified portfolios has historically been limited.

- The economy may look messy, but current data does not indicate that it is falling apart. Recession risks appear manageable, not ominous. Diversification is working, while bonds continue to provide income and stability even as prices fluctuate.

- AI innovation‑driven investment, particularly in areas tied to productivity and efficiency, may continue to be a meaningful long‑term tailwind.

In Conclusion

We build resilient portfolios, rebalance thoughtfully, and stay aligned with long‑term financial goals. Periods like Q1 test confidence, but they also underscore the value of a well‑constructed investment strategy. And just as Ted Williams knew his success came from patience, discipline, and waiting for the right pitch, long‑term investing rewards the same steady approach. This means staying selective, staying focused, and trusting the process. And if you’re thinking about how this applies to your own situation, we’re here to help you make sense of it. Reach out any time.

YCharts ©2026 YCharts, Inc. All rights reserved. The information contained herein: (1) is proprietary to YCharts, Inc. and/or its content providers; (2) may not be copied, reproduced, retransmitted, or distributed; and (3) is provided AS IS with all faults and is not warranted to be accurate, complete, or timely. YCHARTS, INC. AND ITS CONTENT PROVIDERS EXPRESSLY DISCLAIM, TO THE FULLEST EXTENT PERMITTED BY APPLICABLE LAW, ANY WARRANTY OF ANY KIND, WHETHER EXPRESS OR IMPLIED, INCLUDING WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE, ACCURACY OF INFORMATIONAL CONTENT, OR ANY IMPLIED WARRANTIES ARISING OUT OF COURSE OF DEALING OR COURSE OF PERFORMANCE. Neither YCharts, Inc. nor its content providers are responsible for any damages or losses arising from the use of this information. Past performance is no guarantee of future results. YCharts, Inc. (YCharts) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through the application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Bloomberg data provided by Bloomberg. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the FTSE and Russell Indexes. MSCI data © MSCI 2026, all rights reserved. S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

Investment Commentary: Q1 2026

George Padula, CFA®, CFP®

Wealth Manager, Principal

As a native New Englander, I grew up cheering the Red Sox and I am happy to say my daughters do the same.

A good friend and I frequently text about the Red Sox’s chances for the upcoming season. He typically takes a more optimistic view, while I am more realistic about their chances. Either way, the team gives us ample opportunity to cheer the highs and lament the lows.

We both agree, though, that Ted Williams was the greatest hitter of all time. Yes, you Yankees, Giants, Dodgers, and Cardinals fans will put in plugs for DiMaggio, Bonds, Piazza, and Musial. I get it. All are great. But they were not Ted Williams. First published in 1971, his book, “The Science of Hitting”, is still a gem. Williams was disciplined, educated, patient, and focused on the fundamentals. His secret was as simple as “getting a good pitch to hit.” Undisciplined hitters become impatient, and overconfident, impulsively chasing bad pitches, making poor decision after poor decision.

For Ted Williams, a good long-term decision process was the key starting point. It is a lot like investing.

The fundamentals: valuation, diversification, discipline, and risk management are necessary. Good investing requires deep self-awareness, an understanding of constraints, and knowledge of the game being played. These conditions are when the “good investing pitches” start to appear.

The war in Iran and the surrounding regional tensions have made this an undeniably difficult period. But if we are true investors, with a sound long-term process, this conflict alone may not warrant stopping or dramatically changing a long‑term investment plan. Now more than ever, having an investment process matters. Knowing how and why to make investment decisions is as important as the outcomes. Being patient and not chasing bad investments may help support better long‑term outcomes.

Last quarter, I wrote that optimism and skepticism can be both held at the same time. Nothing in the last three months has changed that.

As we head into the commentary, there are really three themes of focus: interest rates, economic growth and market volatility.

Geopolitics and the oil shock: what is different today?

The first quarter reminded investors how quickly markets can flip from optimism to uncertainty. After a strong finish to 2025, Q1 2026 was dominated by geopolitics, specifically the escalating conflict involving Iran, and the resulting shock to global energy markets. While uncomfortable, these events also reinforced why disciplined portfolio construction and long-term focus remain essential.

The dominant narrative of the quarter was the conflict within Iran and its implications for global energy supply. Disruptions and threats around the Strait of Hormuz, a critical artery for roughly one‑fifth of the world’s oil supply, sent crude prices sharply higher with Brent oil surging above $100 per barrel.

These price spikes flowed quickly through the economy, reigniting inflation concerns.

Here in the U.S., the long-term impact from higher prices will likely be muted. According to data from the U.S. Energy Information Administration, petroleum production and exports are far higher now than they ever have been with daily production up 170% vs. 1980 and 40% higher than 1970. At the same time, U.S. crude oil exports have gone from almost nothing twenty years ago to approximately 1.5 billion barrels per year. While this energy transformation gives the U.S. more flexibility, it doesn’t mean that gasoline prices and heating costs won’t increase. Rather, the rate of increase may likely be less than they would have been otherwise.

From an investment perspective, markets can respond in various ways to supply shocks, and energy‑related inflation may moderate as conditions stabilize.

Markets in Q1 were mixed

Looking at the chart below, we see that equity markets started out strong and then pulled back sharply in March with the conflict in Iran. The large cap, tech-heavy S&P 500 declined approximately 4% for the quarter. However, not all markets declined. The Russell 2000 small cap index gained 0.9% and global real estate was up 0.8%. Bonds were mixed as interest rates were both up and down.

International equities were relatively resilient despite the global uncertainty. Over the last 12 months, developed international and emerging market indices outperformed U.S. indices.

Bonds, meanwhile, were challenged as inflation risks pushed yields higher, leaving broad U.S. bond benchmarks flat to slightly negative year‑to‑date.

The returns shown are annualized returns for benchmark indices. Investors cannot invest directly in an index. Unmanaged indices do not reflect management fees or transaction costs. Past performance is not a guarantee of future results. Source: Ycharts. See full disclosures.

Digging deeper, there was a large difference in styles, with the Russell 2000 Value Index (Small Value) outperforming the Russell 1000 Growth Index (Large Growth) as indicated below. This tilt to value began in 2025 with worries about an AI bubble and the technology’s effect on software companies and has continued as the war in Iran boosts value-oriented stocks in energy and defense industries.

Source: Ycharts

Taken together, this all highlights the role of diversification during a time of market stress.

What’s on investors’ minds

Given all this movement across styles, sectors, and global events, it’s natural to wonder what it all means for your portfolio and what questions matter most right now. And if you’re asking yourself some of the same questions we’re hearing from investors, you’re not alone.

These ups and downs and volatility seem out of the ordinary. Should I be worried?

Market ups and downs are a feature of investing, not a flaw. From a longer‑term perspective, these recent market moves are well within historical norms. Pullbacks occur regularly, even in strong market years, and naturally occur amid changing information and sentiment. This chart shows the performance of the S&P 500 (bars) and the largest intra-year decline (dots) each year. The average year sees a stock market drop of -13.5%. However, most years still end in positive territory (see chart below). Volatility is a normal part of investing and investors are often rewarded for staying disciplined through short-term volatility.

Source: Clearnomics

How fearful should we be of a recession? With oil prices increasing, jobs all over the place, and both inflation and rates rising, a recession seems inevitable.

Rising oil prices, mixed job signals, and higher inflation and rates can create a convincing “perfect storm.” But what feels inevitable isn’t always what’s most likely. Recessions are not triggered by headlines.

While the chance of an economic slowdown or mild recession is elevated, the likelihood of a deep, prolonged downturn still appears relatively low. While the above pressure points are real, we are not seeing them at critical levels, and there are multiple relief valves still in place.

The labor market remains strong, without the broad job losses that typically precede recessions. Consumers and businesses are still in solid financial shape, unlike prior downturns. Even with the possibility of higher energy prices, inflation has moderated from its peak, reducing the need for further aggressive tightening.

Our focus isn’t about predicting a recession, but it is about being prepared for one. Going back to our disciplined process: Stay diversified, emphasize quality and resilience, maintain liquidity aligned with your needs. It’s natural to feel concerned, but this is a time for discipline, not reaction. Historically, markets tend to recover before the data improves, so reacting emotionally may be costly.

The economy seems so confusing. How concerned should I be?

It does feel confusing right now, because the signals are mixed. The U.S. economy entered 2026 on solid footing, but expectations are tempered. Consumer spending remains resilient, though hiring may be slowing and the unemployment rate has drifted modestly higher. Inflation remains an uncertain challenge and the Fed signaled a cautious, data‑dependent approach.

In our view, while the picture is more complex than usual, on the whole, it’s not one that currently points to a severe or systemic breakdown.

Interest rates: With so much uncertainty, why isn’t the Federal Reserve cutting rates?

That’s a very fair question, and it gets to the heart of what the Federal Reserve is managing right now. At the start of the year, consensus estimates had the Fed cutting rates a few times in 2026. However they are now in a policy pause, not a policy shift.

The Iranian conflict has clearly increased inflation risks over the short term, and the Fed is signaling a cautious approach. At their March meeting, the Fed took any 2026 rate cuts off the table but noted the longer-term trend of decreasing interest rates remains. It is likely that interest rates will remain unchanged through the end of 2026. Essentially, the two 2026 cuts may be pushed into next year starting with the Fed’s meeting in June 2027. This pause gives the Fed room to maneuver if economic conditions sharply deteriorate.

While higher‑for‑longer rates can create short‑term headwinds for bonds, yields today offer far more income than in prior years, improving long‑term return potential for diversified fixed income.

Key Takeaways for Portfolios

We mentioned at the start that a disciplined process is crucial as we navigate the remainder of 2026. Staying focused, grounded, and aligned with long‑term goals helps put short‑term volatility into context.

In Conclusion

We build resilient portfolios, rebalance thoughtfully, and stay aligned with long‑term financial goals. Periods like Q1 test confidence, but they also underscore the value of a well‑constructed investment strategy. And just as Ted Williams knew his success came from patience, discipline, and waiting for the right pitch, long‑term investing rewards the same steady approach. This means staying selective, staying focused, and trusting the process. And if you’re thinking about how this applies to your own situation, we’re here to help you make sense of it. Reach out any time.

YCharts ©2026 YCharts, Inc. All rights reserved. The information contained herein: (1) is proprietary to YCharts, Inc. and/or its content providers; (2) may not be copied, reproduced, retransmitted, or distributed; and (3) is provided AS IS with all faults and is not warranted to be accurate, complete, or timely. YCHARTS, INC. AND ITS CONTENT PROVIDERS EXPRESSLY DISCLAIM, TO THE FULLEST EXTENT PERMITTED BY APPLICABLE LAW, ANY WARRANTY OF ANY KIND, WHETHER EXPRESS OR IMPLIED, INCLUDING WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE, ACCURACY OF INFORMATIONAL CONTENT, OR ANY IMPLIED WARRANTIES ARISING OUT OF COURSE OF DEALING OR COURSE OF PERFORMANCE. Neither YCharts, Inc. nor its content providers are responsible for any damages or losses arising from the use of this information. Past performance is no guarantee of future results. YCharts, Inc. (YCharts) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through the application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Bloomberg data provided by Bloomberg. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the FTSE and Russell Indexes. MSCI data © MSCI 2026, all rights reserved. S&P data © 2026 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

Follow us on social:

Related Articles:

Talk to an experienced financial planner

Related Articles:

Modera Wealth Management, LLC (Modera) is an SEC-registered investment adviser. SEC registration does not imply any level of skill or training. For information pertaining to our registration status, the fees we charge including how we are compensated and by whom, additional costs that may be incurred, our conflicts of interest, any disclosed disciplinary events of the Firm or its personnel, and the types of services we offer, please contact us directly or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov) to obtain a copy of our disclosure statement, Form ADV Part 2A, and ADV Part 3/Form CRS. In addition, our Privacy Notice outlines how we handle your non-public personal information. Please read these documents carefully before you make a decision to hire Modera, invest or send money.

This material is limited to the dissemination of general information about Modera’s investment advisory and financial planning services that is not suitable for everyone. Nothing herein should be interpreted or construed as investment advice nor as legal, tax or accounting advice nor as personalized financial planning, tax planning or wealth management advice. For legal, tax and accounting-related matters, we recommend you seek the advice of a qualified attorney or accountant. This material is not a substitute for personalized investment or financial planning from Modera. There is no guarantee that the views and opinions expressed herein will come to pass, and the information herein should not be considered a solicitation to engage in a particular investment or financial planning strategy. The statements and opinions expressed in this material are relevant as of the date of publication and are subject to change without notice based on changes in the law and other conditions.

Investing in the markets involves gains and losses and may not be suitable for all investors. Information herein is subject to change without notice and should not be considered a solicitation to buy or sell any security or to engage in a particular investment or financial planning strategy. Individual client asset allocations and investment strategies differ based on varying degrees of diversification and other factors. Diversification does not guarantee a profit or guarantee against a loss.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.