Knowing what to focus on at each point can help make planning feel less intimidating. To bring some clarity to this process, we use an age‑based financial map that highlights the considerations most relevant at different points in your life.

People often worry about whether they’re making the right financial decisions, protecting their families, or preparing well for the future. These concerns are common, and they can feel overwhelming without a clear framework to guide you. Having a structured way to think about your financial life can make a meaningful difference.

In our decades of providing financial planning services to individuals and families, we’ve learned that identifying the issues most relevant at each stage of life helps bring clarity to the process. A client’s age can be one factor that helps highlight which financial planning needs may be most relevant. For example, while a young professional may not need a strategy for gifting assets to heirs, he or she may need to consider how to replace income in the event of a disability.

Over the years, this age‑based financial map has helped many clients understand how insurance, investment management, tax planning, and estate planning needs evolve over time. By viewing these milestones as part of the broader financial stages of life, it becomes easier to see how each step contributes to your overall plan.

What is a long-term financial plan?

A long‑term financial plan is a structured roadmap that helps individuals, families, and businesses organize their financial decisions over many years, often across multiple financial stages of life. It typically includes goal‑setting, saving and investing strategies, risk management, tax planning, and estate considerations. In practice, financial planning for all of life’s stages is one of the most effective ways to carry out this long‑range approach, breaking a complex plan into manageable, age‑appropriate steps.

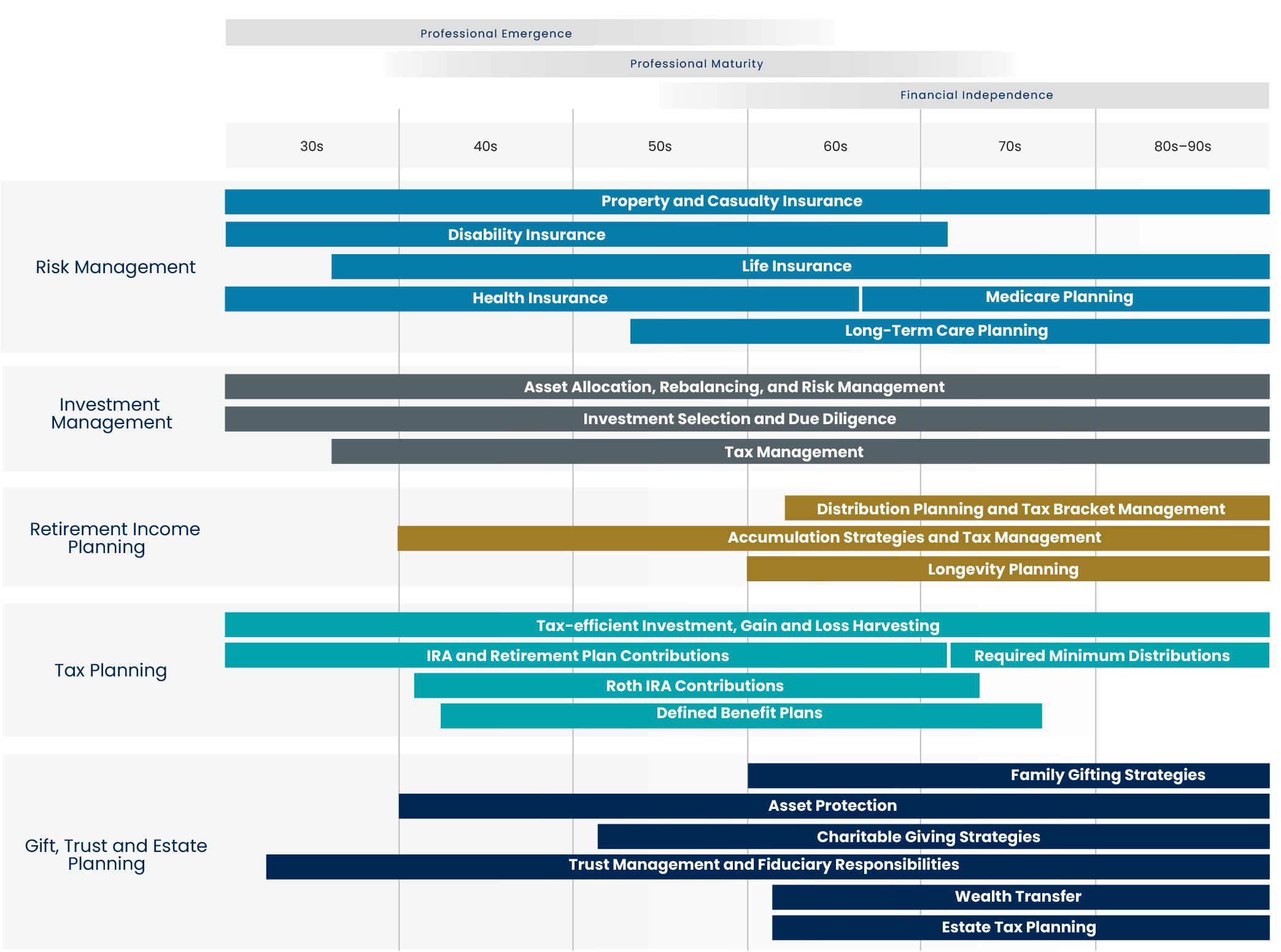

Financial Planning for Life Stages

Below is a breakdown of how these financial planning considerations evolve over time:

In your 30s and 40s

Adequate property, disability, liability, and life insurance are crucial to the protection of your financial future. Determining the best way to take advantage of savings opportunities in IRA and other retirement plan accounts is important. Investing your savings prudently can help you work toward the goals that matter to you. Wills, trusts, and other important estate planning documents also can be critical to providing financial security for your spouse and children in the event of your death or incapacity.

At this stage, long‑term financial planning often focuses on building a strong foundation, protecting income, establishing savings habits, and creating a structure that supports future goals.

In your 50s

At this age you may have accumulated a reasonable amount of assets. As a result, your life insurance needs may have decreased from what they were in your 30s and 40s. However, your disability, liability and property insurance are likely still critical. You also may wish to start considering long-term care insurance. Your income has likely increased, and an effective savings strategy is also very important, as is maintaining a prudent investment strategy for those assets. Careful tax planning can help you make informed decisions about how to maximize your accumulation of wealth to fund your retirement and other financial goals.

This period is often about refining your long‑term financial plan, adjusting insurance, maximizing retirement contributions, and preparing for the transition from accumulation to distribution.

In your 60s

Evaluating your need for long-term care insurance is usually very important at this stage of life. You should evaluate your annual spending and start to consider how you may fund your spending from your investment assets in retirement. Retirement income planning, including the identification of a sustainable withdrawal strategy and the minimization of taxes on that income, can help you make thoughtful decisions about how to use your savings. Roth Conversions and tax bracket-filling strategies may be considered during this period. You also should evaluate when you’d like to begin receiving your social security benefits, as you will generally be eligible for benefits as early as age 62. Since you likely have been building your net worth for a number of years, and your family tree has likely evolved, you may wish to consider re-evaluating your estate plan.

Here, long‑term financial planning becomes more focused on income sustainability, tax efficiency, and preparing for the distribution phase of retirement.

In your 70s

Tax laws require you to start taking annual minimum distributions from certain retirement accounts such as IRAs. Qualified Charitable Distributions (QCDs) is a tax-efficient charitable giving strategy that may fit your situation starting in your early 70s. Developing effective family gifting and wealth transfer strategies may now be of greater importance for you.

This stage often emphasizes managing required distributions, optimizing charitable strategies, and aligning your long‑term financial plan with your legacy goals.

In your 80s and 90s

Maintaining your retirement income through effective investment management and income tax planning still remains a top priority. Achieving philanthropic goals and continuing your wealth transfer strategies may be of increasing priority for many. Maintaining up-to-date durable powers of attorney and health care proxies can help provide your loved ones with the ability to care for you in the event that such care becomes necessary

During these later financial stages of life, planning often centers on preserving financial stability, simplifying decision‑making, and ensuring your estate and healthcare wishes are clearly documented.

Conclusion

Understanding the financial stages of life can make long‑term financial planning feel more approachable. Each stage builds on the last, creating a cohesive path toward your goals. By revisiting your plan regularly and adapting it to life changes, you can maintain clarity and confidence as you move through each chapter of your financial life.

It is hard to make the right financial decisions if you don’t know what actions you need to take. That’s why our age-based financial map can be such a useful resource. By identifying which financial matters are most important to you, you’ll be able to work toward your financial goals more effectively and feel more prepared as your circumstances evolve.