Hopefully, you are taking full advantage of this benefit. If you are, why not take the time to check in on your retirement plan contributions and make certain you make the most of your plan and are on track with your savings goals for the year?

Making the Most of Your Contribution Opportunities?

The 2026 employee contribution limit is $24,500. If you are at least 50 years of age, you can contribute an additional $8,000 catch-up contribution (subject to annual IRS adjustments).

As a result of the SECURE 2.0 Act, an enhanced “super catch-up” opportunity is available for employees aged 60–63. In 2026, the super catch-up amount for this group is $11,250 (replacing the standard catch-up amount for those eligible), if the plan allows.

Important to note, beginning in 2026, individuals earning more than $145,000 (indexed for inflation) in the prior calendar year are required to make catch-up contributions on a Roth (after-tax) basis. However, due to implementation timing, many employer plans may not fully adopt this requirement until 2027.

Consider increasing your contributions to account for this year’s contribution limit increase. Your paystub should tell you what you are contributing so you can evaluate if you will maximize your contributions by the end of the year.

Why Maximizing Contributions Matters

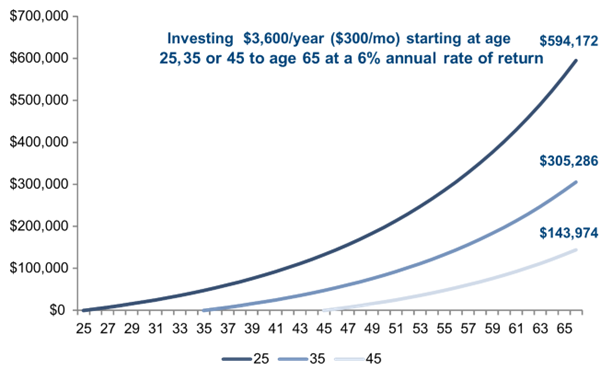

Consistent retirement savings can have a meaningful impact over time. If you do not have the ability within your cash flow to max out your contributions, consider adjusting your budget elsewhere to allow you to increase your contributions. Any increase to your savings will have an impact, especially with the power of compounding interest. The earlier you can start saving the better. See the chart below for an illustrative example on the power of compounding interest and the benefits of saving as early as you can.

Projections are based on assumptions provided by the advisor and are not guaranteed. Actual results will vary, perhaps to a significant degree. The projections are hypothetical in nature and for illustrative purposes only and do not account for fee deductions, commissions and other expenses associated with investing.

Strategies to Help You Maximize Contributions

Some 401(k) plans allow you to deposit a bonus directly into your account. This is a great way to boost your retirement savings without cutting deeper into your regular paycheck. Another strategy is to make certain each paycheck contributes a set amount that will automatically bring you to the annual maximum by the end of the year.

There is also a more immediate benefit to stashing more cash into your 401(k) plan throughout the year. If you are contributing on a pre-tax basis, you are also lowering your taxable income. That means a smaller tax bill when you file your income tax return. Of course, if you are saving on a pre-tax basis, you will pay taxes when you withdraw money from the account in retirement. If you want to avoid the tax in retirement and pay it now, you

can contribute to a Roth 401(k) if your employer offers that option. Speak with your advisor to determine the most appropriate strategy for your circumstances.

What to Consider After Maxing Out Your Plan

If you have additional money, you may be able to save for retirement with these other plans:

- Roth IRA (subject to income limits) or Backdoor Roth IRA

- Traditional IRA (subject to income limits)

- HSA

Other options to consider include paying down debt, contributing to a 529, or adding to an emergency fund.

If you have any questions regarding your investments, elections, or other savings strategies, please do not hesitate to reach out to Modera. We are happy to help.